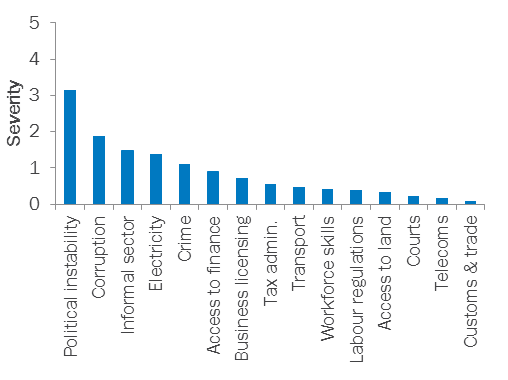

In MENA ES 2013-14, the top three business environment obstacles identified by Egyptian firms were political instability; corruption; and competitors’ practices in the informal sector (Chart 1). Young firms were more often constrained by electricity issues and access to land. There were significant regional differences within the top constraints. In particular, electricity issues were the second most severe constraint in Dakahliya, Gharbiya and Kafr El Sheikh/Menoufiya/Beheira, while firms located in governorates along the Suez Canal complained about customs and trade regulations.

It is not surprising that political instability was the top concern for Egyptian firms in 2013-14 as the economy deteriorated in the wake of the 2011 uprising, along with the developments that took place in summer 2013.

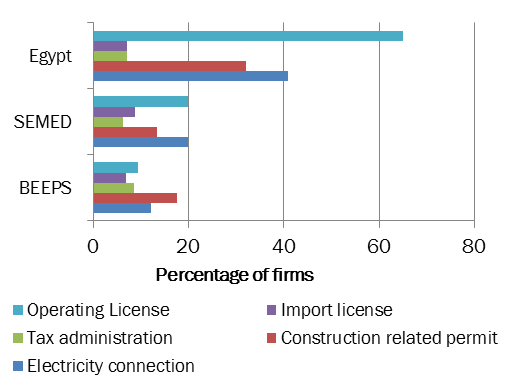

Corruption was the second most severe constraint. The share of firms reporting that an informal payment was expected or requested when obtaining an electrical connection (40.9%), a construction-related permit (32.2%), or an operating licence (65.0%), was the highest in the SEMED region and well above the respective averages for the rest of the EBRD region (Chart 2). Young firms and SMEs were more likely to report that an informal payment was expected or requested. One of the explanations for this could be that the well-established firms have been able to build local networks and connections with various authorities and/or service providers.

Competitors’ practices in the informal sector were the third major concern. Almost half of the firms reported competing against unregistered or informal firms, compared with roughly 40% in SEMED and the rest of the EBRD region. The informal sector in Egypt has developed over the years as a response to an increasingly complex bureaucratic system coupled with unclear rules of enforcement and insufficient legal protection. Burdensome laws, red tape and high costs of licensing and registration discouraged particularly SMEs from formally registering. Estimates suggest that the informal sector constitutes around 40% of GDP and 66% of total non-agricultural employment in the private sector.

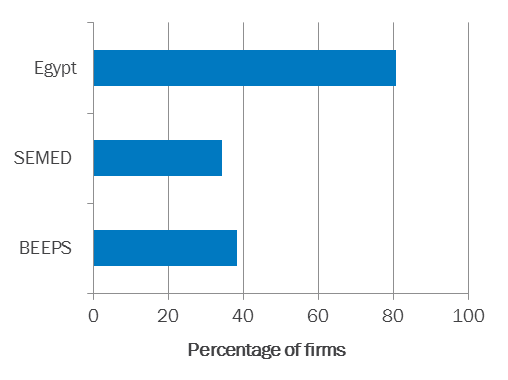

The unreliable supply of electricity has also been a major constraint for businesses, including younger ones. More than 80% of firms say they experienced power outages (Chart 3), on average more than 20 in a typical month, particularly over the summer. The estimated losses of Egyptian firms from power outages amounted to 13.6% of total annual revenue, significantly above the SEMED average of 7.7% and the average for the rest of the EBRD region (5.0%). Power outages have become more frequent in recent years due to the continuous rising demand for electricity, a shortage of natural gas (the main input fuel for the power sector), an outdated and inefficient power sector, coupled with poor levels of maintenance standards leading to power plants producing below capacity. In addition, oil and gas exploration activities in Egypt have dropped significantly since 2011 due to the ongoing political turmoil as well as the significant arrears owed by EGPC, the Egyptian national petroleum holding company, to foreign oil and gas companies.

Despite the finding that only 12.5% of firms had an overdraft facility and only 6.0% of the firms had received a loan or a line of credit from a bank, with more than 85% of firms that needed a loan either discouraged from applying or rejected when they did (the worst indicators among the SEMED countries), access to finance was not among the top three binding constraints in Egypt. This indicates that while access to finance remains very limited compared with other SEMED countries and the rest of the EBRD region, firms were even more concerned about other aspects of the business environment.

The survey data show substantial variation in the quality of the local business environment across governorates.(1) The table below shows the three most binding constraints as perceived by representative firms in each of them. As expected, political instability and the related economic uncertainty affected firms across the country as a whole. In some regions, firms complain about elements of the business environment that do not, on average, rank highly as constraints in Egypt as a whole. For example, firms located in governorates along the Suez Canal (Port Said, Ismailia and Suez – the international ports for trade) considered customs and trade regulations to be the second most binding obstacle. They do not feature among the top three obstacles in other regions and were in last place in Egypt as a whole. Due to the rise in the activities of violent groups, port authorities have strengthened safety measures. In addition, according to a report by the World Bank, administrative and regulatory guidelines appear to be the biggest hurdle for Egyptian businesses planning to export their products abroad or import from other countries. In Egypt, for example, firms need to fill out on average eight documents to export and 10 documents to import, above the MENA average of six documents for imports and eight for exports.

There are some common business environment features across the regions: political instability was named as the most binding constraint by all. The results also suggest that neighbouring regions often have very different profiles in terms of their business environment. For example, firms in Alexandria named competitors’ practices in the informal sector and corruption as the second and third most binding constraints, while firms in the neighbouring Kafr el-Sheikh/Menoufiya/Beheira region ranked electricity issues before competitors’ practices in the informal sector. These cities experienced power outages of longer duration than in Cairo or Alexandria.

With the exception of Dakahliya, where more than 60% of firms reported needing a loan, and almost all of them – 97.5% – were credit-constrained, access to finance was not among the top three business constraints. However, in most governorates the share of credit-constrained firms was above 84%. The only exceptions were Red Sea/Matrouh/Wadi al Jadid/Sinai (22.7%), Qualyubia (72.6%) and Cairo (73.7%).

The elements of the business environment that do not appear to be among the top three binding constraints in any of the Egyptian regions are: business licensing and permits, labour regulations, workforce skills, transport, tax administration, access to land, courts and telecommunications. However, some of these were among the top three binding constraints for specific types of firms.

For young firms, customs and trade regulations were among the top three binding constraints in Alexandria, Cairo, Dakahliya, Red Sea/Matrouh/Wadi Al Jadid/Sinai and Sharqia, but not in governorates along the Suez Canal, where they were more concerned about electricity and corruption. In Upper Egypt, young firms were more concerned about transport than electricity, while business licensing and permits, corruption and access to land were reported to be particularly binding for young firms in Damietta. In the cotton-processing region of Kafr el-Sheikh/Menoufiya/Beheira, young firms were most concerned about corruption and labour regulations. The latter was the third most binding constraint in Dakahliya, one of the major agricultural governorates in Egypt.

Electricity issues were among the top three binding constraints identified by large firms in all regions except Alexandria, Sharqia and Upper Egypt. Large firms also named corruption as a more binding constraint than SMEs in Dakahliya, Damietta, Gharbiya, Kafr el-Sheikh/Menoufiya/Beheira, and Qualyubia.

Firms in the services sector were most concerned about competitors’ practices in the informal sector (rather than political instability) in Alexandria, Damietta, Dakahliya, Kafr el-Sheikh/Menoufiya/Beheira, Qualyubia and Upper Egypt.