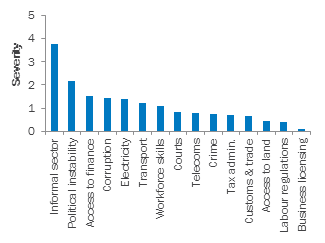

In BEEPS V, the top three obstacles that Cypriot firms identified in the business environment were competitors’ practices in the informal sector; political instability; and access to finance (see Chart 1). Issues with electricity and transport were more problematic for large firms. In the northern part of Cyprus, political instability was the most severe constraint for firms and workforce skills the third most severe.

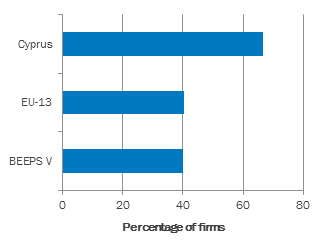

About two-thirds of Cypriot firms reported competing against firms in the informal sector, exceeding the average for the EU-13 countries covered in BEEPS V by almost 27 percentage points (see Chart 2). Young firms are less likely to compete with firms in the informal sector than old firms are, though still more likely than their EU-13 counterparts. Informal sector practices may include practices by registered firms, such as paying part of wages informally and not declaring them to the administration, thus contributing to informal employment. According to some estimates, Cyprus’s informal economy accounts for 26% of GDP, compared with 18% for the EU-27.

It is not surprising that Cypriot firms named political instability as the second most severe constraint as the island remains in effect divided. Efforts towards reunification continue, having received a boost after the leaders of the Greek Cypriot and Turkish Cypriot communities agreed on 11 February 2014 on the text of a joint declaration for resuming fully fledged negotiations on a comprehensive political solution. Elevated political sensitivities on both sides are accompanied by controversy regarding property rights or titles which dates back to the armed conflict.

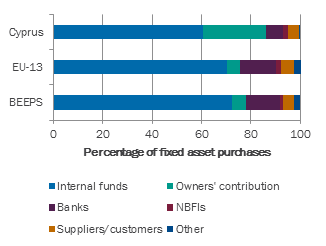

Though some of the Cypriot firms surveyed complained about access to finance, many had reasonably good access, compared with the rest of the countries in the EU-13. 61.7% of them had a line of credit or a loan, in contrast with 45% in the EU-13, and these loans were on average more than twice the duration of those in the EU. However, Cypriot firms were less likely to purchase fixed assets, and when they did, 25.2% of their value was financed from owners’ contributions or issuing new equity shares and only 6.9% by banks, in contrast to the EU-13 averages of 12.1% and 14.4%, respectively (see Chart 3). Their complaints about access to finance could be linked to the fact that the banks have significantly tightened lending criteria since the start of the financial crisis. Prior to the crisis, many firms could get a loan for all project costs on the basis of a business plan and collateral priced at an optimistic, post-completion project value.